by Ed Blount and Dan Hammond

On April 2nd, 2026, an effusion of data from a daily trove of U.S. regulatory filings will create resources to drive many new use cases for artificial intelligence in capital markets. A clear opportunity exists in securities finance, where practitioners have repeatedly stated that major IT investments will be needed to comply with the many new regulatory mandates. “Black box” AI platforms may seem a ready solution but can also create nightmares for client reviews and lawsuits.[1]

In our opinion, public data can clarify the rational limits of influence for predictive artificial intelligence. The best courtroom-ready models will display an audittrail based on the replication of critical decision parameters and vectors from past markets. Vendor data in securities finance may be more timely and deeper than the public releases but, for judicial purposes, the public data will provide foundational evidence for the “bounded rationality” of decision-makers, as defined by the late Herbert Simon, Nobel Laureate and the father of Artificial Intelligence.

Maintaining a Training Dataset as an Audit Trail for the Courtroom

As we have recently explained, forecasts of financing fees and inventory buffers can be made using regulatory filings to gauge the parameters that have guided or influenced the past actions of traders, head traders, and business heads in capital markets divisions. To embed their insights, AI models must be trained with sequences of concurrent time series for each market participant.

To demonstrate, we have adapted a very large dataset from Tidal Markets LLC and created a prototype AI model for securities finance. Our prototype can be used to customize models for participants to rely on predictions of fees for stock loans and buffers for lendable inventories, in the following fashion:

- Traders' past insights are defined as 10- and 20-day rolling averages of key metrics, such as fees, tickets, and amounts, and factored as indexes of current financing trends for an individual security issue, sector or market. For example, the range of borrowers' fees are considered to trend as negotiated spreads to adjusted balances posted by FINRA under Rule 10c-1 (read more here) on trading days over the last two to four weeks;

- The Head traders' predictive dataset compares indexed trends of key traders' metrics to those of the prior quarter to derive the weights of tensors that connect the parameters, based partly on implied gains and losses. The prototype is used to document predictions of the degree to which the desk is likely to meet its annual forecast in business plans for risk-adjusted returns on capital ("raroc");

- The Management dataset in our prototype considers conditions year-to-year in allocating capital and adjusting raroc the desk’s performance for seasonality, pandemics, and corporate actions, among key benchmarking factors.

For any given market condition, every model in securities finance should be trained with layers of economic capital allocations and predicted regulatory claims on capital. Our prototype predictiveAI model analyzes the current flows of market capital in the context of prior allocation decisions made at each level of trading operations. Fees and new loans are two measures of experience in the market, but inventory buffers and economic capital are the primary limiting factors. If head traders do not allocate enough of their scarce capital resources to traders, then opportunities, no matter how attractive to traders, will be allowed to slip by.[2]

Predictive AI is essentially a sentiment model which tries to replicate lenders' and borrowers' decisions in context of their insights and outcomes, by measuring the loans of securities against collateral. On the assumption that most borrowers are short sellers, our prototype assumes that each level of trading operation “satisfices,” in Simon’s term, its allocated capital for the most efficient, regulatory-compliant opportunities.

Using Regulatory Capital as the Final Constraint on Trading Operations

In global banks whose primary supervisors have adopted Section MAR12.4 of the Basel capital regulations, each business head is defined as an account with claims on a proportional amount of capital from the firm's balance sheet to be used to conduct trading operations. From a regulatory standpoint, the trading book has a different set of restrictions from the banking book. Each head trader in the group is allocated part of that capital for management of a group of traders.

Each head traders' desk is capitalized for operations involving a set of similar securities. The head trader generally decides which securities are traded by the individual traders. Each trader considers the prices and fees of assigned securities in comparison to a rolling average of recent market factors, as described in the bullets above.

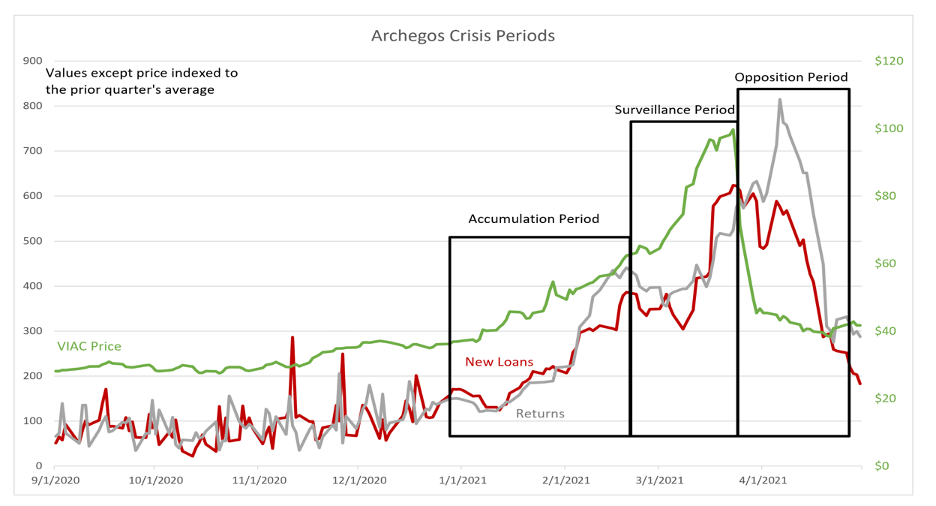

Predictions will be accurate to the extent that parameters of other issues change in similar degree to other stressed securities on trader watch lists. In our prototype, the slope and standard deviation of their indexed values is one test we are using to identify issues of significant interest. To illustrate, we have again selected the CBS Viacom (VIAC) manipulation by Archegos of September 2020 through March 2021 that depleted the capital of Credit Suisse Bank. We have used details from the SEC’s complaint against Archegos to guide our modeling.

“MARKET POSSE” ACTION PERIODS:

ACCUMULATION, SURVEILLANCE, AND OPPOSITION

In the Archegos manipulation, short sellers realized that the VIAC stock price was out of control early, but potential profits were too low to commit much capital as shown by 'new loan units'. In each of the three action periods, as shown in our September 28 article, the time-series horizon of the human decision-makers is a variable marked by parametric thresholds. For example, a rising slope of the 20-day rolling average for VIAC vectors of share prices, fees and new loans was the marker for the transition from a watch list entry for short sellers to a target issue. We defined that as the Accumulation period when capital was being allocated to traders by short sellers in order to accumulate borrowed shares in the expectation of a price drop.

In the Archegos manipulation, short sellers realized that the VIAC stock price was out of control early, but potential profits were too low to commit much capital as shown by 'new loan units'. In each of the three action periods, as shown in our September 28 article, the time-series horizon of the human decision-makers is a variable marked by parametric thresholds. For example, a rising slope of the 20-day rolling average for VIAC vectors of share prices, fees and new loans was the marker for the transition from a watch list entry for short sellers to a target issue. We defined that as the Accumulation period when capital was being allocated to traders by short sellers in order to accumulate borrowed shares in the expectation of a price drop.

Each of the parameters can change in significance from time to time. As a result, depending on circumstances, there are different weights for each of the periods, i.e., Accumulation, Surveillance and Opposition. The predictiveAI model derives its tensor strengths as weighting factors using the training dataset. Each backpropagation in the recursive regression analysis of the training program results in changes for the weights of each parameter. Therein lies the essential value of every generative AI model, i.e., its ability to re-weight its parameters as accurately as possible so as to minimize the "loss function" of its predictions at every step of the time series.

Training datasets should be used to condition the AI model to a multi-dimensional matrix of decision factors -- in the best case using fees and new loans made in past markets by each human decision-maker -- in order to predict the optimal allocation of capital. Inventory buffers are a derivative of those decisions, but fees are both an input to and output from the model. That's because human decisions are not made in a vacuum. There are other influences on the market conditions within which the trained model will predict future market conditions and recommend reactions. Deeper levels of learning in securities finance, including predictions of fees, will require ticket level data for the training datasets.

Training datasets should be used to condition the AI model to a multi-dimensional matrix of decision factors -- in the best case using fees and new loans made in past markets by each human decision-maker -- in order to predict the optimal allocation of capital. Inventory buffers are a derivative of those decisions, but fees are both an input to and output from the model. That's because human decisions are not made in a vacuum. There are other influences on the market conditions within which the trained model will predict future market conditions and recommend reactions. Deeper levels of learning in securities finance, including predictions of fees, will require ticket level data for the training datasets.

[1] Holistic views of decisions made at all management levels were at the center of many lawsuits that followed the 2007-2008 Great Financial Crisis. Fiduciaries had to prove their actions were reasonable and served their clients’ best interests in context of their contractual policies and procedures.

[2] That was the situation on Black Monday 1987 when stock index futures traded off basis to the cash markets for an extended period. Traders simply did not have enough capital to bring the markets back into sync even though they saw the arbitrage trade of a lifetime slipping away.